Mortgage in Principle vs Full Application: what’s the difference and when to get one is one of the most common questions for homebuyers in the UK. Understanding the distinction can save you time, reduce stress and improve your chances of securing your dream home.

In this guide, we’ll break everything down in simple terms so you know exactly when and why to use each.

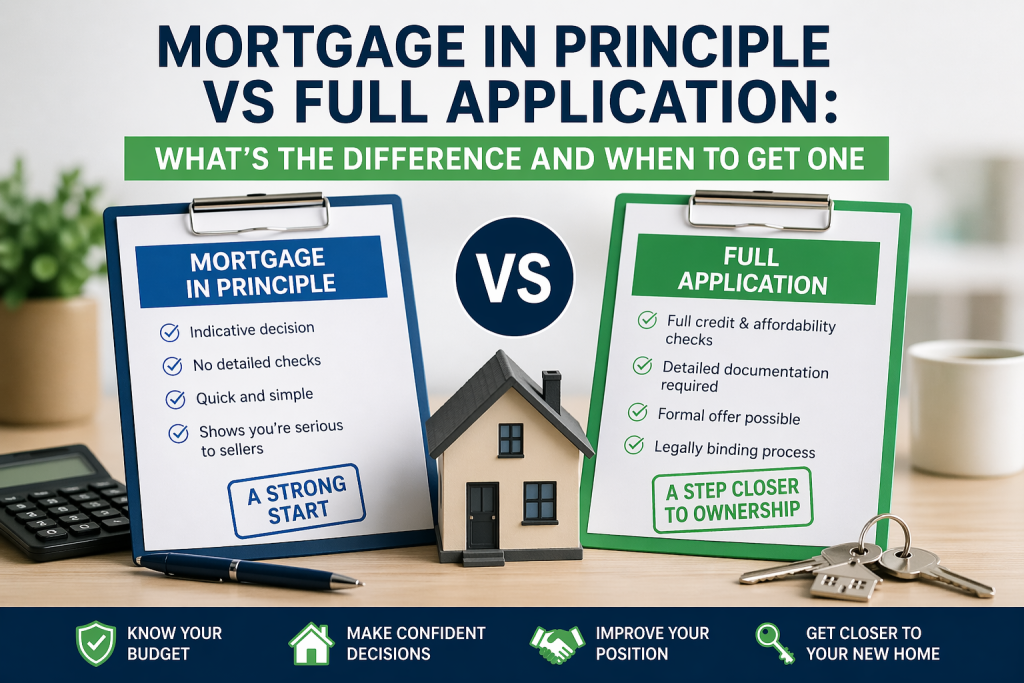

🤔 What is a Mortgage in Principle?

A Mortgage in Principle (also called a Decision in Principle or DIP) is an initial indication from a lender of how much they might be willing to lend you.

It’s based on basic information such as:

- Your income

- Your employment status

- A soft or light credit check

It’s not a guarantee, but it gives you a realistic budget.

✅ Benefits of a Mortgage in Principle

Helps you understand your borrowing power

Makes you more attractive to sellers

Speeds up the buying process

Often required by estate agents before viewings

⚠️ Limitations of a Mortgage in Principle

It’s not a formal offer

Based on limited checks

Can expire after 30–90 days

📄 What is a Full Mortgage Application?

A full mortgage application is the formal process where a lender thoroughly assesses your finances before approving your loan.

This is where things get serious.

📑 Documents Required

You’ll usually need:

3 months’ payslips or accounts (if self-employed)

Bank statements

Proof of ID

Credit history details

🏦 What Lenders Check

- Full credit report

- Affordability under stress tests

- Income stability

- Property valuation

This is the stage where your mortgage is either approved or declined.

⚖️ Mortgage in Principle vs Full Application: what’s the difference and when to get one

Let’s break down Mortgage in Principle vs Full Application: what’s the difference and when to get one clearly:

| Feature | Mortgage in Principle | Full Application |

|---|---|---|

| Purpose | Estimate borrowing | Secure mortgage |

| Checks | Basic | Detailed |

| Speed | Fast (minutes) | Slower (days/weeks) |

| Guarantee | No | Yes (if approved) |

| Credit Impact | Usually soft | Hard check |

In short:

- A Mortgage in Principle helps you start

- A Full Application helps you finish

⏰ When Should You Get a Mortgage in Principle?

You should get a DIP before you start house hunting.

This ensures:

- You know your budget

- You avoid wasting time

- You can act quickly when you find a property

Estate agents often prioritise buyers with a Mortgage in Principle.

🏁 When Should You Make a Full Mortgage Application?

You should only submit a full application after your offer is accepted.

This is because:

- It involves a hard credit check

- It commits you to a lender

- It requires full documentation

Timing is critical.

🚀 Step-by-Step: From Mortgage in Principle to Full Application

Here’s how the process typically works:

- Get a Mortgage in Principle

- Start property viewings

- Make an offer

- Offer accepted

- Submit full mortgage application

- Property valuation and Underwriting

- Mortgage offer issued

💡 Common Mistakes to Avoid

- ❌ Applying for multiple mortgages in a short time

- ❌ Changing jobs before completion

- ❌ Taking on new debt

- ❌ Overestimating affordability

Avoiding these mistakes can improve your approval chances significantly.

📊 Final Thoughts

To summarise:

- A Mortgage in Principle is your starting point

- A Full Application is your final approval step

Understanding this ensures you move through the home-buying process confidently and efficiently.

🔗 Helpful Links

- Loan to Value Explained — The Complete Guide to Smarter Mortgage Decisions

- Why Use a Mortgage Broker? Top 7 Reasons to Get Expert Mortgage Advice

- AIPs, DIPs and MIPs- What’s the Difference?

- 7 Key Costs To Budget For When Buying A Home

- MoneyHelper (UK government-backed)

- FCA

🚀 Book a Free Consultation Today

Ready to take the next step?

👉 Book a free consultation with our mortgage experts today and get personalised advice tailored to your situation. Whether you need a Mortgage in Principle or you’re ready for a full application, we’ll guide you every step of the way.